Table of Contents

Let’s just call it like it is. Your debt is a burden.

You need to get rid of it once and for all. I am going to show you how to pay off debt the fast way. The amazing thing is, you will have options.

I still remember the day I got my shiny new credit card in the mail.

It was my first card that I got to “build up my credit”. So I decided to run that bad boy through a few registers. I bought some groceries, gas, and some other things I needed.

About a month later the credit card statement came in the mail. I spent $350. At the very bottom of the page, the credit card bill said in bold letters. Amount due: $24.

I could not believe what my eyes were telling me. I could spend $350 and only have to pay $24? This has to be too good to be true.

Of course, it was. As I kept reading, I realized that I would have to pay 18% interest on the remaining $326 balance. Did the credit card company think I was a moron?

Unfortunately they did. They trap people into this scheme over and over.

Debt is a National Crisis

Debt has become extremely easy to obtain. You wouldn’t be pushing that car without easy financing. It is something that is promoted to us as “Good”.

There is currently more debt than ever before. In the U.S. alone there is:

- Over 8 Trillion in home mortgages

- Approaching 2 trillion in student loans

- Over 3 trillion in Consumer debt and Auto Loans

Here’s the average amount of debt for each age group:

- Under 35: $67,400

- 35–44: $133,100

- 45–54: $134,600

- 55–64: $108,300

- 65–74: $66,000

- 75 and up: $34,500

Money Is A Powerful tool – Use It Wisely

One thing that I just cannot understand is the fact that people would rather have material things that, in essence, make them work much harder and longer than they have to. Debt is dumb, borderline insane. It has to be addressed in a blatant manner.

If you are currently taking on debt, specifically consumer debt, then you need to stop (in the name of love) now. No ifs ands or buts. It must end, you’re destroying your life one transaction at a time.

I talk about empowering your life through money. It has nothing to do with pinching pennies, nickels, dimes, but using money to put you in the driver’s seat.

Money has the capability of changing your life for the better. It gives you the opportunity for pure freedom. But if you are carrying debt then you are going in reverse.

It is crippling to you and your future.

If you are already in debt, and reading thus far was an extreme bummer, cheer up because I will show you how to develop a plan. A plan that will bring you back to freedom.

Reasons Debt Brings You Down

Debt takes away your Cash

Without debt, you can keep your cash for the things you care about. Your cash is what can bring you value. It allows you to put your money towards the things you want. Even if you live a lavish debt lifestyle, the more debt you take on, the more your income is eaten away.

Debt Takes Away Your Opportunity

Every dollar that you have to pay back with interest is money you could be using to increase your balance sheet. If you are slaving away to pay off your car loan, when you could be investing in index funds, you are losing the opportunity that those investments could bring forth.

You are Enslaved to Your Job

Debt requires you to have a job. You have to work so you can pay for your debt. You can no longer make choices that align with your values.

Debt Increases Stress and Anxiety

Debt can make you feel like an entire mountain is sitting on your chest. This pressure can build. Studies show that you actually feel the same emotions as an addict: Guilt, shame, remorse, and helplessness.

If You Are Already in Debt Stop Digging

If you are already in a hole, the first thing that you must do is stop digging.

If your debt is growing every month, you need to find out why. You cannot keep consuming above your means. The number one way to win at this game we call money is to spend less than you make.

It’s a simple concept yet most people do the opposite. Let’s crush your debt once and for all.

How to Decide if You Should Pay off Debt

Many people wonder if they should even pay off certain debts. I know I ask myself the same question.

The quick answer is that it depends. Mainly on your interest rate and comfort levels. My mortgage is only 4%, but I make 8% on average in an index fund, wouldn’t my money be better served in the market?

This is a valid point and something that needs to be weighed out. Here is my rule of thumb on interest rates when it comes to paying off debt.

- If the debt is 3% or less, pay off the debt slowly, and invest your hard-earned dollars.

- If your debt is between 3%-5% use your best judgment for your situation.

- If your debt is over 5% pay it off!

If debt brings you anxiety or worry. Then just get rid of it, no matter the interest rate. You want to have a clear mind so you can make good, sound financial decisions.

Allowing something like debt to take away your mental health is not an option. Just crush it, so you can have a clear mind.

The Fast Way to get Rid of Your Debt (The Debt Wrecking Ball)

Debt Is Like Miley Cyrus – You need to come in like a wrecking ball.

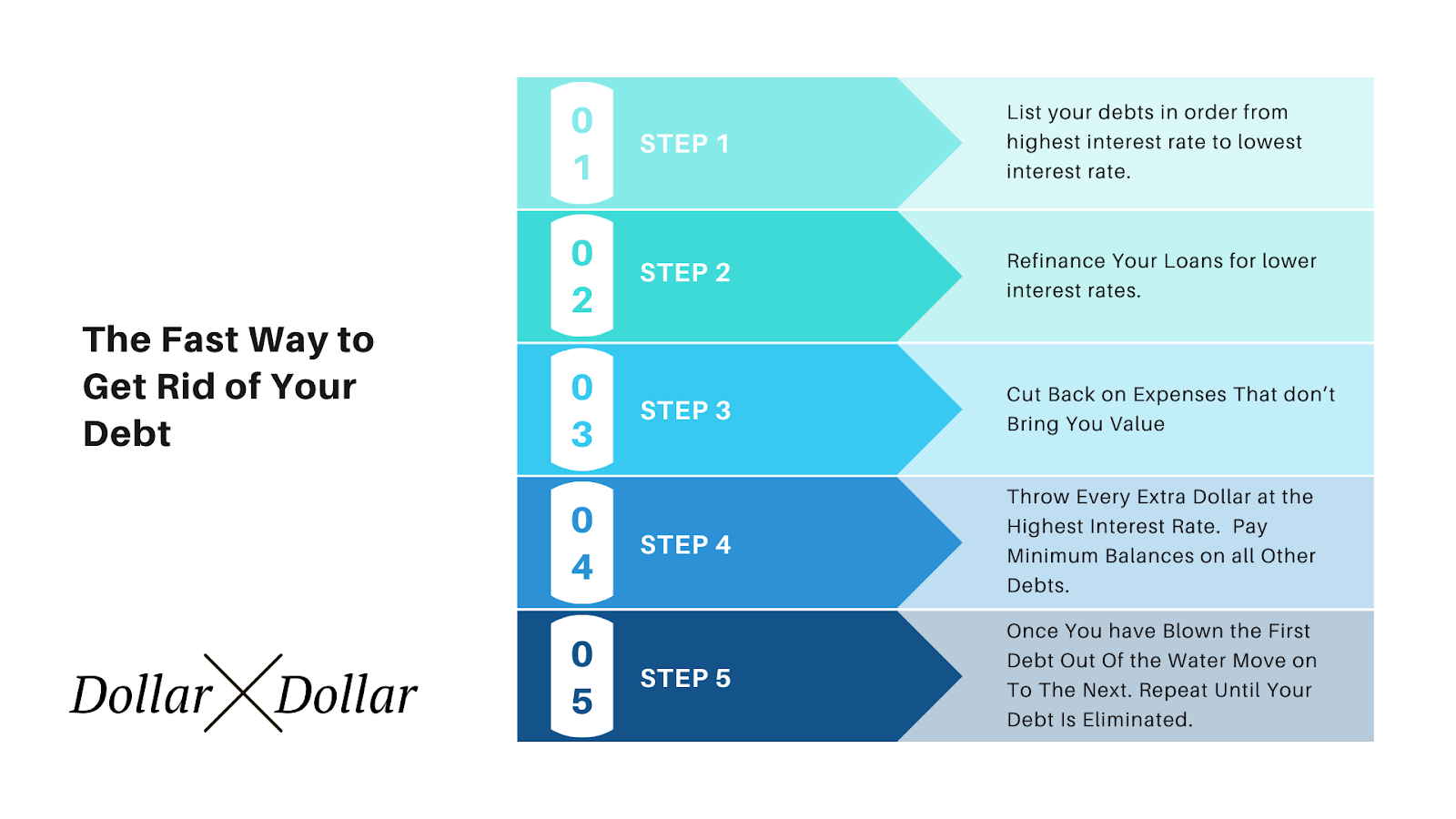

The fastest way to get rid of your debt is simple. You list your debts from the highest interest rate to the lowest.

Step 1: List your debts in order from highest interest rate to the lowest interest rate.

Listing your debts from highest interest rate to lowest interest rate will give you an attack plan. This allows you to get rid of your debt faster. Identity your highest interest rate debt as the one you will pay down aggressively first.

Step 2: Refinance Your Loans for lower interest rates.

Consolidate and refinance when it makes sense. If you have a high interest rate, then you will get ahead by refinancing. If you are trying to pay off a small amount of debt (less than $10,000), skip this step and put all your focus on getting rid of that nagging debt.

Step 3: Cut Back on Expenses That don’t Bring You Value

Cut back on all the splurges that don’t bring you any value. Eat out less. Spend less on groceries. Cut out the excess. Do whatever you can to get your expenses down so you can get rid of this debt.

At the same time, sell off items in your house that you don’t want/need anymore. Throw the extra money at the debt.

Step 4: Throw Every Extra Dollar at the Highest Interest Rate. Pay Minimum Balances on all Other Debts

Pay the minimum balances on all of your debts except the one you want to get rid of. Then go after your priority debt (the one with the highest interest rate). Take every extra dollar and chuck it at that debt. You will begin to see that remaining balance fall. Let those small wins motivate you.

Step 5: Once You have Blown the First Debt Out Of the Water Move on To The Next. Repeat Until Your Debt Is Eliminated

After you have eliminated the highest interest rate debt, move on to the next highest interest rate. Once the debt is gone, have a party. Then shift that money to investments so you can pursue financial independence.

The Alternative Option – The Debt Snowball

The debt snowball is not my first choice because it is a slower way to pay down debt. There is no denying that it has worked for many people. Which is why it has to be proposed as an option.

When tackling debt, understand that personal finance is 80% behavior and 20% head knowledge. The second option is that we attack our debt from a psychological perspective.

How the Debt Snowball Works

Go at the debt with the lowest balance first. This approach will give you the feeling of a small win and give you a feeling of control (Dave Ramsey brought this to the forefront).

Start by listing your debts in order from the least to greatest. It could be something like:

$700 Medical Bill

$4,200 Credit Card Bill

$9,000 Car Loan

$19,000 Student Loan

Make the minimum payment on all the debts, then attack the smallest one first. Something like the medical bill can be paid off in a month or two.

Once that first debt is paid off, you take that extra money and go after your next debt, the credit card bill. Pay off the credit card bill then take all that money and roundhouse kick the car loan.

By now you will be a black belt in debt karate and you can face the grandmaster, the student loan. The reason why this works is that you are freeing up your minimum payments on other debts (by paying them off like a boss) and moving them towards your next victim, I mean debt.

What is Good Debt?

Companies will try to sell you on debt. They have gotten so good at promoting debt, that they have led people to believe there is something called good debt. There is no such thing as good debt. It doesn’t exist.

Debt can be used cautiously as a tool. Only for those who can truly handle the payments. Here are some of the categories people call good debt:

Home Mortgages

Mortgages are the highest personal debt item in the U.S. They are a tool that will allow you to buy a home that you can afford. What many people do is buy too much house that they cannot afford.

They would rather be miserable and add a few extra bedrooms they will never use. Seek the least house that meets your needs, instead of the most house you can afford.

To avoid this debt trap, aim to keep your mortgage payment 25% or below. Even better, keep it below 20% and invest the extra cash that comes your way.

Student Loans

Student loans are the newest form of “good debt” that is causing our younger generation to be chained down. The amount people borrow has become a massive problem. They borrow this money at a young age. Unfortunately, public high schools don’t teach personal finance. So they are handing out debt to people without any knowledge of exactly what they are doing to their finances.

It makes you think.

If you can, avoid student loans at all costs. Work while in school and take an extra year so you can balance the two.

If this is not an option for you, then take as little as possible. Student loan interest rates shock me when I see them. It’s no wonder people can never pay them down. You have a 7% interest rate working against you.

There’s no doubt that education is the way to get a good job. Just try not to start your financial life standing in a ditch.

Business Loans

Many businesses borrow money to accelerate growth. Used wisely this is exactly what will happen. They can buy more inventory, assets, or expand their enterprise.

Business loans used poorly are the source of crushing a business. Your business must earn money to pay back those debts. If you have a business, make sure you take on dent in a cautious manner. Otherwise, just pay cash and budget accordingly.

Kill your Debt or Debt Slowly Kills You

You have to have the desire to annihilate your debt. The mentality of an assassin to destroy this freedom sucking leech from your life. If you are constantly feeding into your wants (eating out regularly, consistently buying clothes, still going on vacations, etc.), then you are going to have a hard time paying off your debt.

These things are fantastic if you find value in them, and should be added to your life. But, they are a much more appropriate reward for someone who is debt free.

If you want it bad enough, even a huge sum of debt can be paid off in a year or two. Then, indulges that matter to you can be enjoyed responsibly without adding fuel to the fire.

If you are still living above your means while in debt, it is devastating to your finances.

It’s like taking your hard earned money, dumping it in a bucket, and riding a roller coaster while trying to keep all your money in that bucket. You will save a few dollars here and there, but the majority will go to your debtors waiting below.

You Need to Reward Your Future Self

The continuation of debt will only cause your future self to work harder and live in stress longer. Every interest dollar that you pay to the credit card company is stealing dollars away from your hard earned efforts. This makes your debt an immediate emergency.

Your Money Can Work Much Harder Than You Ever Can.

Once your debt is paid off, have a party. Play some Earth, Wind, and Fire and celebrate. You, my friend, are now about to begin your journey to building wealth. Your debt steals away the ability to put your dollars to work for you, they instead work against you. You can now work toward building something great for your future. Your goal is to avoid ever letting debt creep back into your life and moving forward. You can now pay yourself first instead of throwing your money down the interest rate toilet. In turn, you can drive those interest rates in your favor by making smart, sound, investing decisions.

Sum it Up

If you are in debt, you have made a mistake. This can actually be helpful because you can learn a valuable lesson. Those who succeed, learn from their mistakes and those who fail to build on their mistakes. Your debt is a tidal wave of an emergency. Don’t try to keep up with your friends, do what is best for your situation. Spend less than you make, and invest the rest soundly.

Andrew is the host of The Personal Finance Podcast, a show that is changing the way you think about your money. His primary goal with the podcast is to bring as much value as possible to his listeners.

Andrew's favorite free financial tool he's been using since 2014 to manage his net worth is Personal Capital. Each month he uses their free Investment Checkup tool and Retirement Planner to track his investments and ensure that he's on the fast track to financial freedom.

His favorite investment platform is M1 Finance, a site that allows him to build a custom portfolio of stocks for free. It has no trading fees and is his preferred way to invest without having to lift a finger.

- Who is Eligible for an FHA Loan? - November 10, 2020

- How to Write a Check: A Step by Step Guide (With Examples) - November 6, 2020

- How to Buy Vanguard Index Funds - October 14, 2020